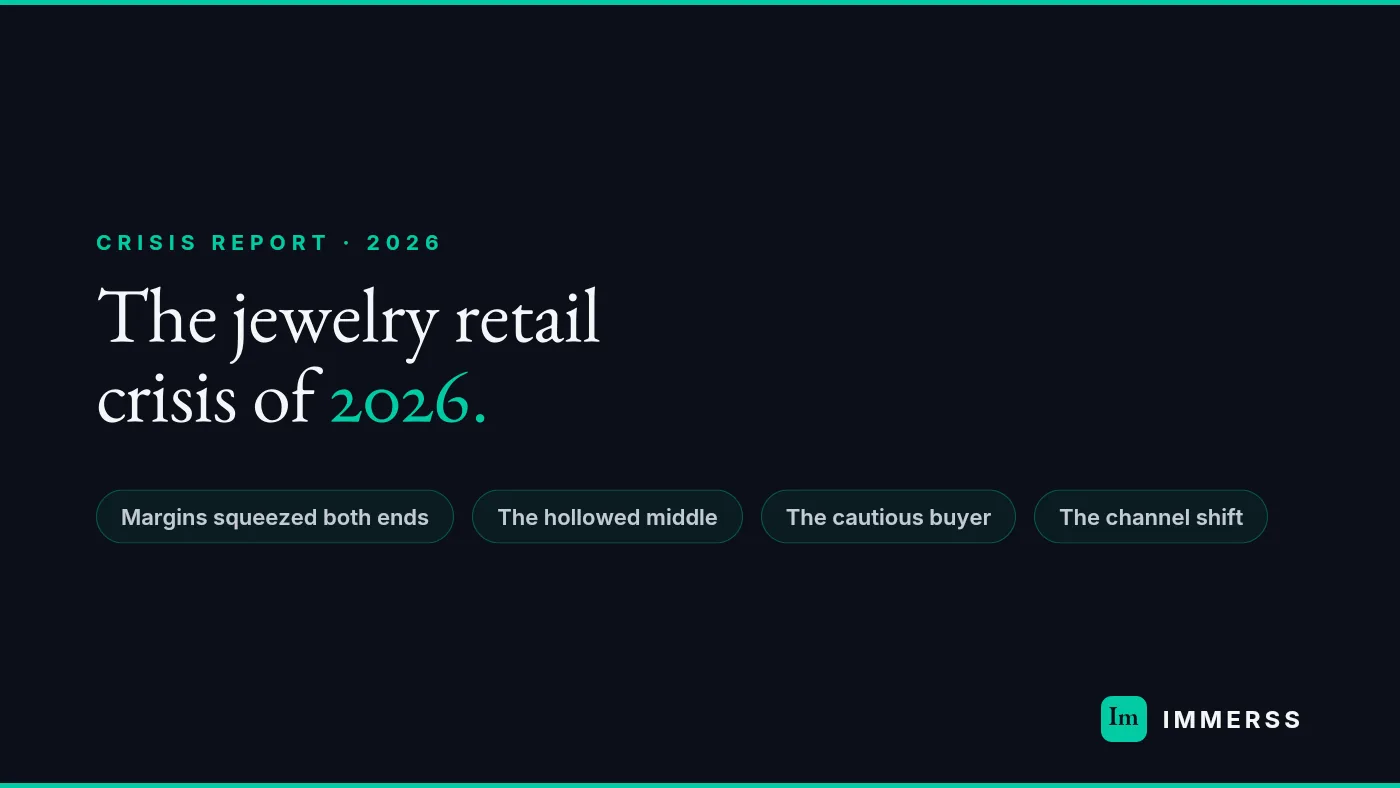

Jewelry retail in 2026 is facing a perfect storm: margins squeezed by lab-grown diamonds and volatile gold prices, the independent mid-market hollowed out between luxury houses and discounters, a more cautious high-ticket consumer, and demand shifting online where jewelers convert poorly. No single pressure is fatal; the danger is that they’ve converged at once. This guide explains what’s driving the crisis and, more importantly, the one strategic move that separates the jewelers who get crushed from the ones who come through stronger.

The short version: every front of this storm punishes the same thing — competing as a commodity — and rewards the same thing — competing as a trusted relationship.

Is jewelry retail in crisis in 2026?

Jewelry retail is under genuine, converging pressure in 2026 — a “perfect storm” rather than a single crisis — but it is sorting the industry, not ending it. Several pressures that jewelers have each weathered before have arrived simultaneously and reinforce one another: margin compression, a splitting market structure, a more hesitant consumer, and a channel shift online. The result isn’t uniform decline; it’s a sharp divide between jewelers competing on price and product (who are being crushed) and those competing on relationship and experience (who are consolidating). Whether 2026 is a crisis or an opportunity depends almost entirely on which side of that divide a jeweler is on.

What’s causing the jewelry retail crisis in 2026?

The 2026 jewelry retail crisis is caused by four pressures converging at once: margin compression, the hollowing of the mid-market, a cautious high-ticket consumer, and the shift of demand to online channels where jewelers convert poorly. Each is survivable alone; together they compound — thin margins meet a hesitant buyer (tempting margin-killing discounts), while the channel shift moves demand to the exact place jewelers are weakest. The reason it deserves the name “perfect storm” is this mutual reinforcement: it isn’t four problems to solve in sequence but one interlocking system, where the obvious fix for any single front (discount to move stock, cut costs and wait, chase cheap online traffic) tends to worsen the others. The sections below break down each front and how they feed one another.

Why are jewelry margins under pressure in 2026?

Jewelry margins are under pressure in 2026 because they’re being squeezed from both ends of the core product at once. From one side, lab-grown diamonds have commoditized the stone — quality is visually indistinguishable, prices have fallen, and the diamond that anchored jeweler margins for a century no longer commands what it did. From the other side, gold prices have climbed and stayed volatile, raising the cost of the metal jewelers work in. Cheaper stones and costlier metal compress the margin from both directions simultaneously, on the very product meant to carry the business. The instinctive response — discounting to keep volume — only accelerates the squeeze.

Why is the independent jeweler getting squeezed in 2026?

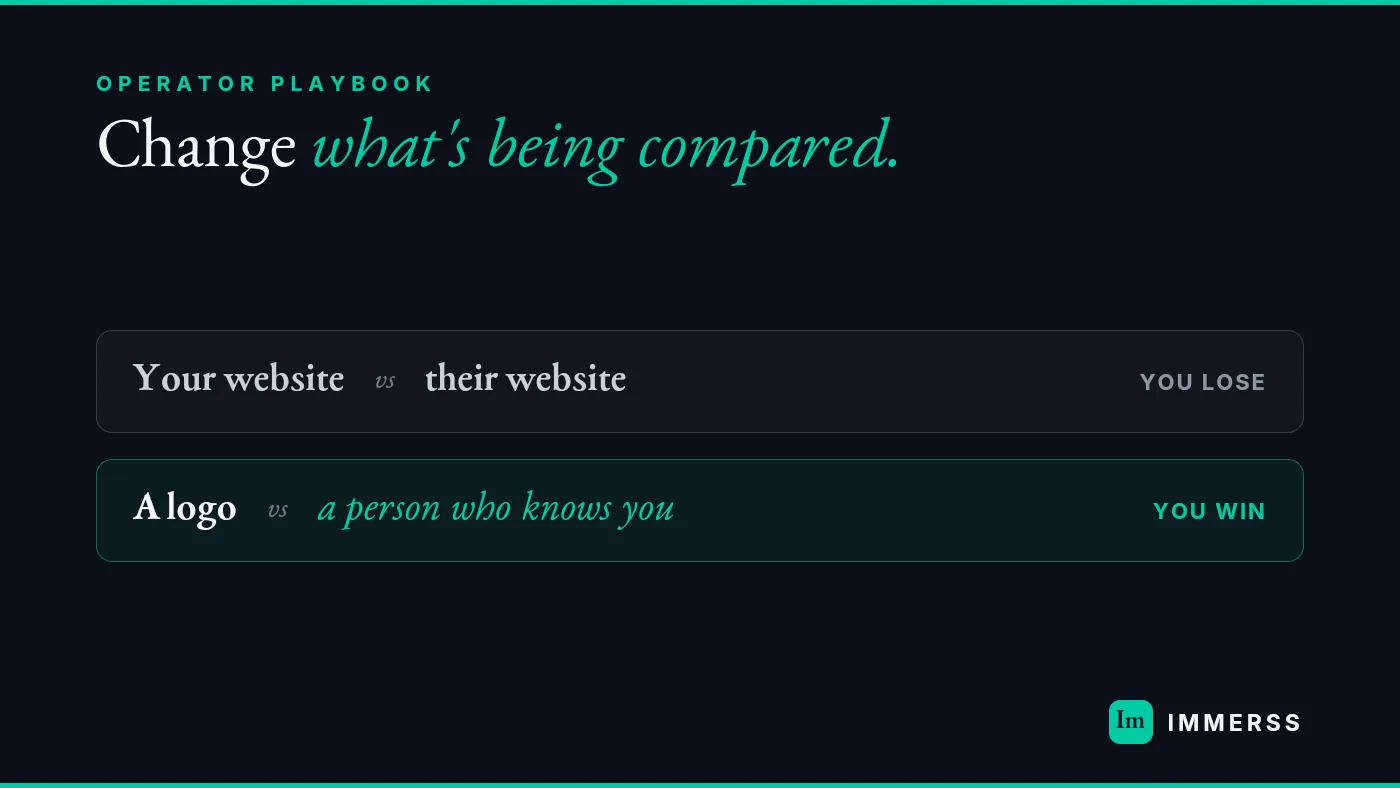

The independent jeweler is getting squeezed because the market structure is splitting and hollowing out the middle they occupy. At the top, global luxury houses pull further upmarket on brand and scale, capturing buyers who buy the name. At the bottom, marketplaces, lab-grown direct-to-consumer brands, and discounters compete ferociously on price, capturing buyers who buy on cost. The independent fine jeweler — neither a global brand nor a discounter — sits in exactly the position the market is emptying. Trying to escape by competing on price (against discounters) or brand (against houses) leads into the strengths of larger rivals. The only defensible position is the one neither end can copy: a genuine, personal, trusted relationship.

How is the cautious consumer affecting jewelry sales?

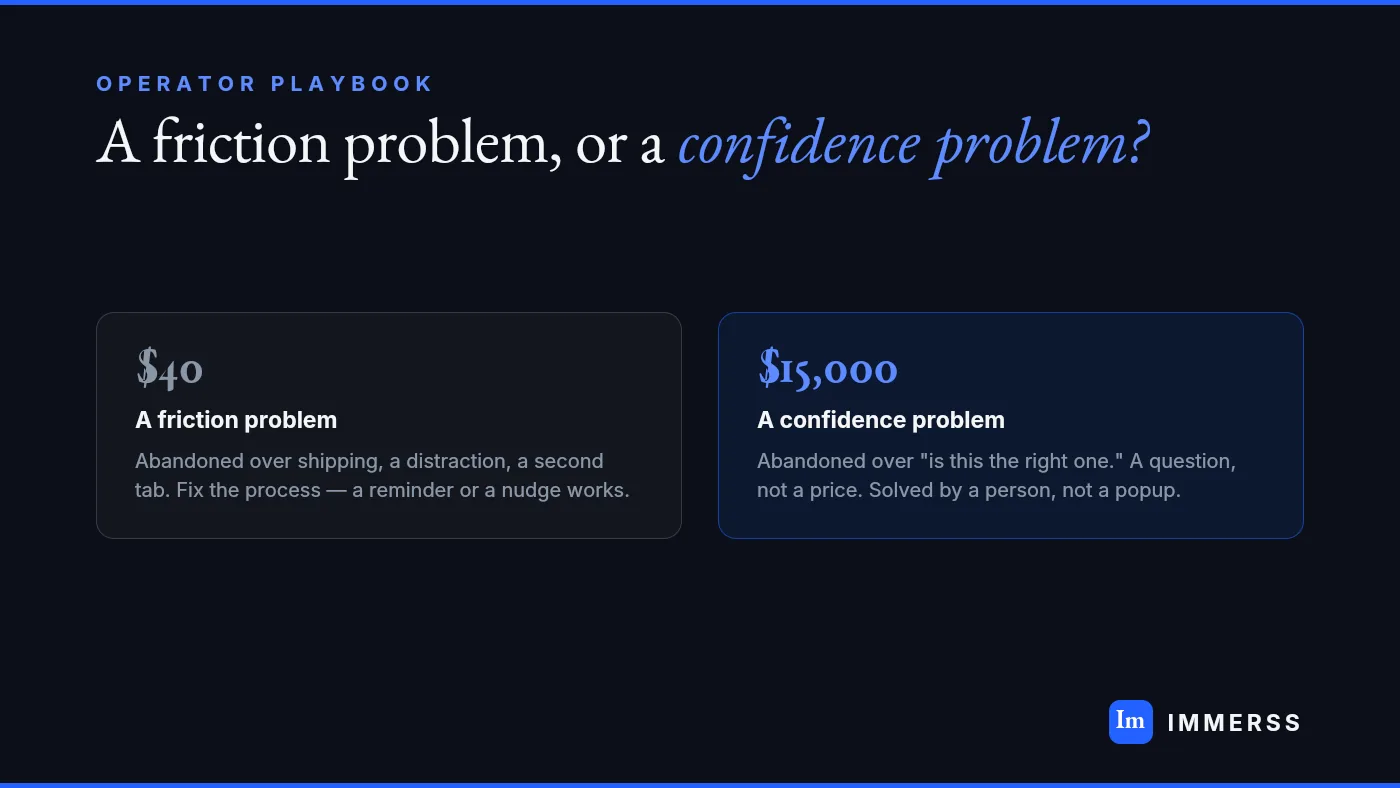

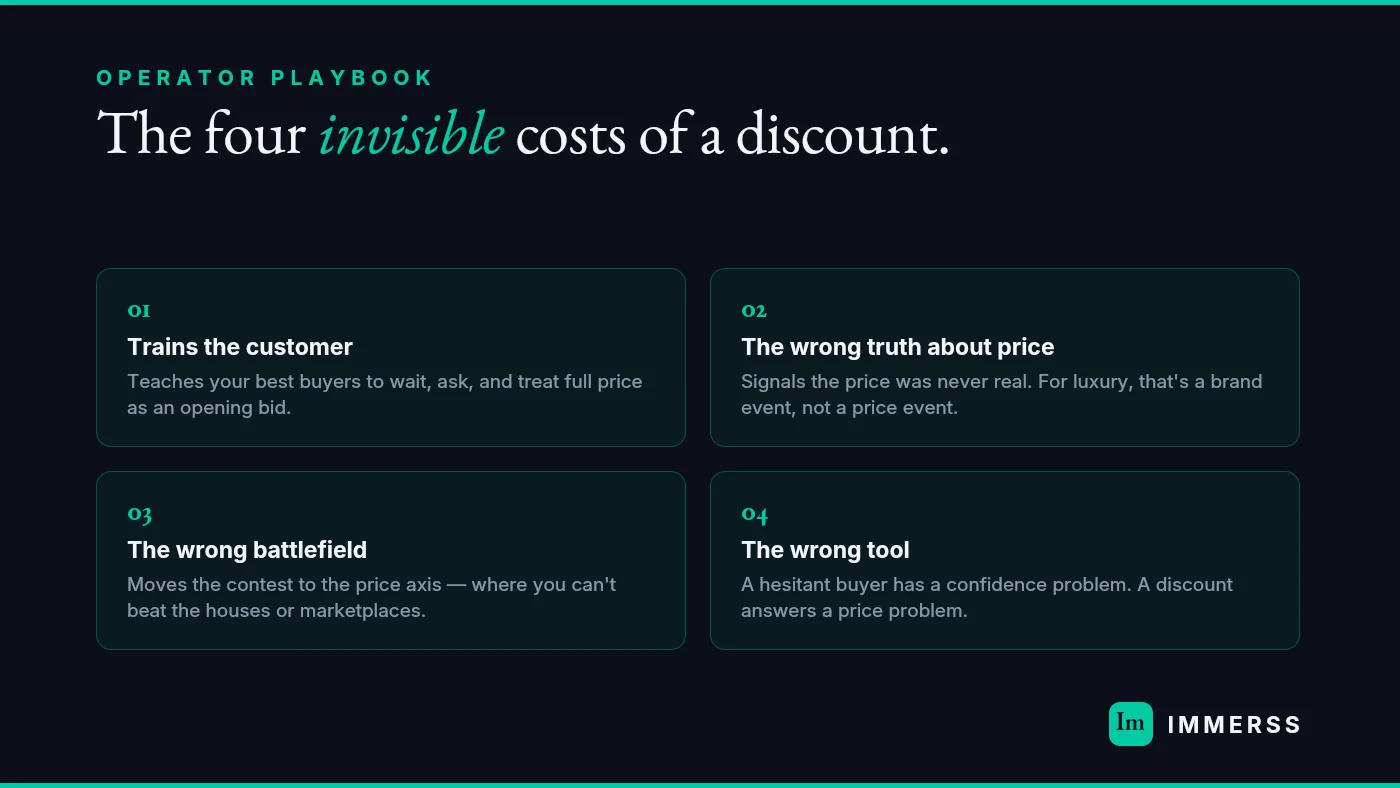

A more cautious consumer is lengthening and stalling high-ticket jewelry sales rather than eliminating them. Economic uncertainty makes buyers more deliberate about exactly the discretionary, emotionally-weighted, five-figure purchase jewelers depend on. People still get engaged, mark anniversaries, and buy meaningful pieces — but they take longer, hesitate more, and need more reassurance before committing. The practical effect is that more deals stall at the threshold, lost not to a competitor but to “let me think about it.” This is a confidence problem, not a price problem, which is why discounting fails to fix it and guidance does — a markdown answers an objection the buyer didn’t have while leaving the real one untouched. (See how to stop discounting and close at full price.)

Why is the channel shift a threat — and an opportunity?

The channel shift is a threat because demand is moving online, where most jewelers convert a fraction of what they convert in store — and an opportunity for the same reason. Discovery and consideration keep migrating to short-form video and AI search while foot traffic softens and acquisition costs rise, so more of the buying journey happens on a website that converts poorly. But jewelers convert poorly online not because people won’t buy jewelry online — they will — but because the online experience lacks the advisor who drives in-store conversion. Restore that advisor online and the channel shift flips from the front that sinks you to the one that carries you. (See why your online conversion lags your in-store rate.)

The fault line: commodity or relationship

Every pressure in this storm sorts along a single fault line. Lab-grown commoditizes the stone, so selling on the stone loses and selling on guidance holds. The middle hollows, so competing on price or brand gets crushed while competing on relationship holds ground neither end can reach. The consumer turns cautious, so self-service fails to reassure while guidance converts. The channel shifts online, so showroom-only selling loses while bringing the guided experience online captures migrating demand. Four fronts, one fault line: the commodity position (price and product — what the storm is destroying the value of) versus the relationship position (trust, guidance, experience — what the storm is concentrating value into). The storm doesn’t sink jewelers at random; it sinks the commodity side and lifts the relationship side. This is also why piecemeal responses fail and a positional move succeeds: because all four pressures sort along the same line, a single decisive shift to the relationship side answers all of them at once, whereas fighting each front on its own terms (matching prices, cutting costs, chasing cheap clicks) keeps you on the side the storm is punishing.

How do jewelers survive the 2026 retail crisis?

Jewelers survive the 2026 crisis by decisively moving from the commodity side of the fault line to the relationship side — now, while it’s a choice rather than a forced evacuation. The mistake to avoid is treating this as four separate fire drills; because all four pressures sort along one line, the move is positional, not tactical. You’re not patching leaks one at a time — you’re sailing the boat to the side of the storm that lifts rather than sinks. Concretely:

- Protect margin through guidance, not discounts. Meet the cautious buyer with a person who builds confidence to buy at full price, rather than a markdown that buys the sale at the cost of the business.

- Reframe the commoditizing product. Treat lab-grown and the volatile-priced gold piece as a decision a confused buyer wants an expert to guide them through, not a price war to lose.

- Lean into the relationship the middle uniquely owns. Compete on the genuine, personal, trusted relationship neither the discounters nor the houses can replicate — the kind of 1:1 clienteling that turns a single sale into a returning, referring customer.

- Bring the showroom experience online. Restore the advisor in the channel demand is moving to — an AI sales agent that engages and qualifies high-intent shoppers, handing them to live one-to-one consultation.

This is exactly what a live commerce platform is for: it isn’t a single tool but three modules working together — an AI Sales Agent that engages and qualifies high-intent shoppers around the clock, Clienteling that turns those moments into 1:1 live co-shopping and outbound relationships, and Video Commerce (live shopping events, shoppable video, and a guided PDP) that brings the showroom to wherever the buyer is. Together they make the relationship side Human, Personal, and Measurable — the three things the commodity side can never be.

Worked example: discounting vs. guiding through the storm

Here’s a calculation you can redo with your own numbers. Take a jeweler facing the margin squeeze, selling pieces at a $6,000 AOV on roughly 40% gross margin ($2,400 gross profit per sale):

- Discount to survive: cut 15% to move inventory and close hesitant buyers. The $6,000 sale becomes $5,100, and the discount comes straight off profit: gross profit falls from $2,400 to ~$1,500 — a 38% cut in profit per sale — while training customers to wait for markdowns. To stand still on total profit, you now must sell far more units into a cautious market.

- Guide to survive: hold the $6,000 price and add a consultation that lifts conversion on high-intent shoppers. One additional full-price sale per day that would otherwise have stalled adds $2,400 of gross profit — the equivalent of recovering the profit lost on ~1.6 discounted sales, at full margin, while strengthening the relationship instead of eroding it.

The math is stark: in a margin squeeze, discounting cuts the profit on every sale you were already making, while guidance adds full-margin sales you were otherwise losing. One path makes a bad situation worse on every transaction; the other compounds in your favor and deepens the relationship at the same time. Swap in your own AOV, margin, and conversion to see the gap for your store.

Is your store on the right side of the fault line?

Run this filter:

- Shopify Plus, 50K+ monthly visits, AOV $500+ (decisive at $5,000+).

- You’re feeling the margin squeeze from lab-grown and gold, and tempted to discount.

- You’re a mid-market independent — not a global house, not a discounter.

- Your online conversion badly trails your in-store conversion.

If two or more are true, the storm is bearing on you — and the move to the relationship side is the survival path.

What jewelers should measure through the crisis

Measure the things that prove you’re on the relationship side, not the commodity side:

- Full-price conversion vs. discount dependency — are you holding margin through trust?

- Consultation conversion and share of high-AOV sales via guidance — is the converting mechanism online?

- Repeat-purchase rate and customer lifetime value — is the relationship compounding?

- Online-vs-in-store conversion gap — are you capturing the migrating channel?

Watch these instead of the metrics that flatter you in calm conditions; in a storm, they’re the early signal of which side of the fault line you’re drifting toward.

The 60-day pilot, on us

The fastest way to move to the right side of the fault line is to put a guided experience in front of your high-intent shoppers and measure what it does to full-price conversion. That’s what the pilot is for.

We run a structured 60-day pilot, on us — an AI sales agent engaging and qualifying high-intent jewelry shoppers, live one-to-one video consultation as the selling mechanism, and measurement around full-price conversion, AOV, and the in-store-vs-online gap. You change no platform and risk no margin to find out what the relationship side does for your store. Documented Immerss outcomes include materially higher conversion, meaningfully larger average orders, and recovery of a significant share of abandoned carts — framed as benchmarks, not promises. Book a demo to scope it for your store.

FAQ: the jewelry retail crisis 2026

Is the jewelry industry in trouble in 2026? Parts of it are, but it’s a sorting rather than a collapse. Jewelers competing on price and product are being squeezed hard by lab-grown commoditization, the hollowed mid-market, and a cautious consumer; jewelers competing on relationship and guided experience are consolidating. The same forces are punishing one group and rewarding the other.

Why are jewelry margins shrinking? Margins are squeezed from both ends: lab-grown diamonds have commoditized the stone and lowered prices, while gold prices have climbed and stayed volatile, raising material costs. Discounting to maintain volume accelerates the squeeze rather than relieving it.

How can independent jewelers compete in 2026? By competing on the one thing neither discounters nor luxury houses can copy: a genuine, trusted, personal relationship and a guided buying experience. Competing on price or brand leads into larger rivals’ strengths; competing on relationship holds defensible ground.

Should jewelers discount to survive the downturn? Generally no. On high-AOV goods, hesitation is usually a confidence problem, not a price problem, so discounting cuts margin without fixing the real obstacle and trains customers to wait for markdowns. Guidance that builds confidence to buy at full price protects margin and the relationship.

How do jewelers sell more online in 2026? By restoring the advisor online. Jewelers convert poorly online because the experience is self-service; adding a guided, one-to-one consultation (often fronted by an AI sales agent that qualifies shoppers) brings the in-store conversion mechanism to the channel where demand is now moving.

See the pilot for merchants: landing.immerss.live Agency partner program: partners.immerss.live

Immerss is a luxury live commerce platform — AI sales agents and one-to-one video consultation for fine jewelry, watches, and high-AOV retail, built on Shopify Plus.